Text by Jonathan Morris, specialist broker at John Lamb Hill Oldridge.

If you have significant assets, it is likely that you will want to pass these on to your family at some point. In recent years, the UK tax authorities have been taking an increasing share of this intergenerational wealth. The latest figures from HM Revenue & Customs (HMRC) show that between April 2022 and October 2022, estates paid £4.1 billion in Inheritance Tax (IHT), £500 million higher than in the same period a year earlier. The chancellor’s recent decision to freeze the threshold at which IHT is payable until 2028, is also likely to result in more individuals paying tax.

One method you can use to ensure you pass on your wealth without losing 40% in IHT is to make lifetime gifts. If your own parents have yet to consider transferring their wealth, this is also something you may want to discuss with them.

The rules surrounding IHT are complex, for example, if a donor dies within seven years of making a gift, there could still be a significant tax liability on that gift.

You may have to sell family assets to pay an Inheritance Tax bill.

Imagine a scenario where you, or your parents want to pass on a valuable gift. Not only does this reduce the value of an individual’s estate as part of a longer-term tax planning strategy, but it also gives the donor the opportunity to see the benefit the gift gives in their lifetime. The gift could be a property, a piece of artwork or another family heirloom.

If the donor were to die within seven years of making the gift, IHT of up to 40% could still be payable on the value of the gift.

If the gift is made in cash, it can be more straightforward to set aside a portion of the cash for seven years in case of any tax bill. However, this is not always as simple as it seems, as often the beneficiary would like to use the entire sum as down payment on a property.

Equally, if a chattel is gifted and the donor dies, your only option could be to sell the asset itself to find the capital to pay the IHT.

Consequently, in the seven-year period after making a gift it is vital that enough liquid assets are kept to cover a tax liability should it arise. One simple way to do this is to procure cost-effective life insurance which would cover the potential liability. This ensures that the recipient of the gift isn’t forced to retain 40% of the cash gift or forced to sell the chattel in order to pay an IHT bill if it falls due.

The insurance mirrors the IHT liability on a gift and is designed to ensure that the bill can be paid, enabling the entire value of the gift to pass to the intended beneficiary with no strings attached. In the event the donor dies, it also enables surviving family members to pay any outstanding IHT and proceed swiftly with an application for probate.

The cost of the insurance will depend on the age of the donor, their health and the amount of cover needed to protect the gift.

How this approach can benefit your family?

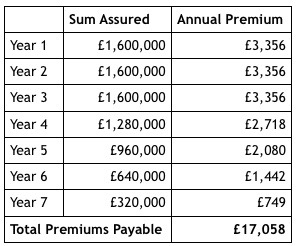

As an example, we recently assisted a 59-year-old client who was gifting a £ 4 million property, in London, to his daughter for use as her family home.

If the father were to die within seven years, his daughter would be liable to pay the IHT due on the gift. This property had an initial liability of £1.6 million which would start to taper 3 years after the gift is made. In this instance, the daughter would not have had enough liquid assets to cover this potential IHT bill. Consequently, if her father had died within seven years there would have been a real possibility that the property would have been sold to fund the IHT liability.

To avoid this the client made the decision to insure the gift. Ultimately, this approach means that the gift is a “closed deal” and the daughter will have the necessary funds available to pay the tax and retain the asset.

In the first three years, the indicative annual cost of this protection was around £3,350. This reduced in line with the IHT liability after year 3, as shown in the table below.

The total cost of the insurance over the seven years equates to just 0.49% of the total value of the gift made.

There are other tax implications that need to be considered when gifting assets, such as Capital Gains Tax (CGT), however gifting assets to younger generations during an individual’s lifetime is often an efficient planning strategy.